Markaðsvirði íþrótta & Úti í Evrópu, Miðausturlöndum og Afríku (EMEA) er 12,04 milljarðar evra árið 2021 og er búist við að hún fari yfir 13,18 milljarða evra árið 2022. Þessi skýrsla mun túlka árangur íþrótta & Útivörur á evrópskum markaði frá mörgum sjónarhornum og leiðbeina seljendum til að meta að fullu þróun vinsælra evrópskra flokka.

Efnisyfirlit:

1. yfirlit yfir evrópskar íþróttir & Útivöru markaður

2.. Neytendaþróun

3. vinsælir flokkar

4.. Svæðishagkerfi evrópskra íþróttamarkaðar

5. Samkeppnislandslag evrópskra íþróttamarkaðar

6. Vaxtarstig evrópska íþróttaiðnaðarins árið 2022

- Yfirlit yfir evrópskar íþróttir & Útivöru markaður

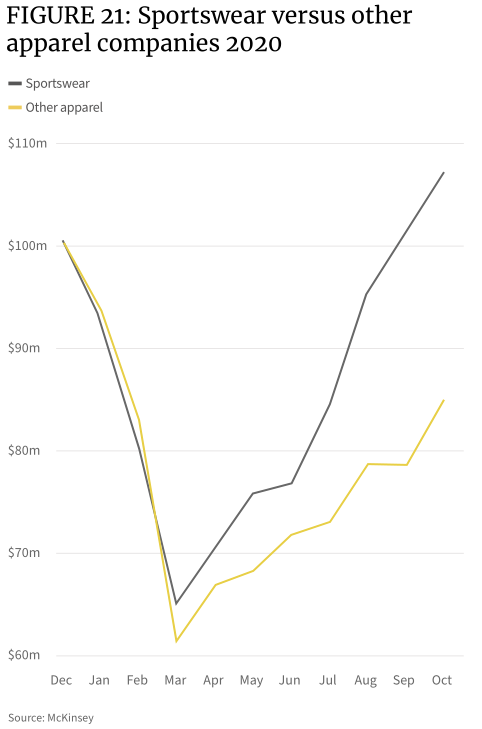

Faraldurinn er án efa sterkasta aðstoðin við aukningu á sölu íþrótta & Útivörur. Í mars 2020 dreifðist faraldurinn til Evrópu og ekki var hægt að framkvæma íþróttaíþróttir og íþróttir innanhúss. Þetta leiddi til grundvallarbreytingar á íþróttakjörum allrar álfunnar í Evrópu árið 2020 og 2021. Áhrif af ferðatakmörkunum og tóku þátt í þessum tveggja ára sölu vetraríþróttafatnaðar með færri skíðum og öðrum vetraríþróttum.

Fleiri neytendur snúa sér að persónulegri hreyfingu, þar á meðal jóga og Pilates. Meðan á faraldrinum stendur eru ekki mörg verkefni sem fólk getur farið út í framkvæmd, aðallega gönguferðir og hlaup, sem hefur skapað góðan markað fyrir útivist og göngubúnað. Íþróttamarkaðurinn í íþróttum og tómstundum, sem sameinar einkenni jógafatnaðar, íþróttafatnaðar og frjálslegur fatnaðar, hefur orðið heitur flokkur þegar fólk vinnur að heiman og tekur netnám. Innkaup á netinu, sem eina leiðin fyrir neytendur að versla þegar múrsteins- og steypuhræraverslanir eru lokaðar, hefur opnað sölu vegna faraldursins.

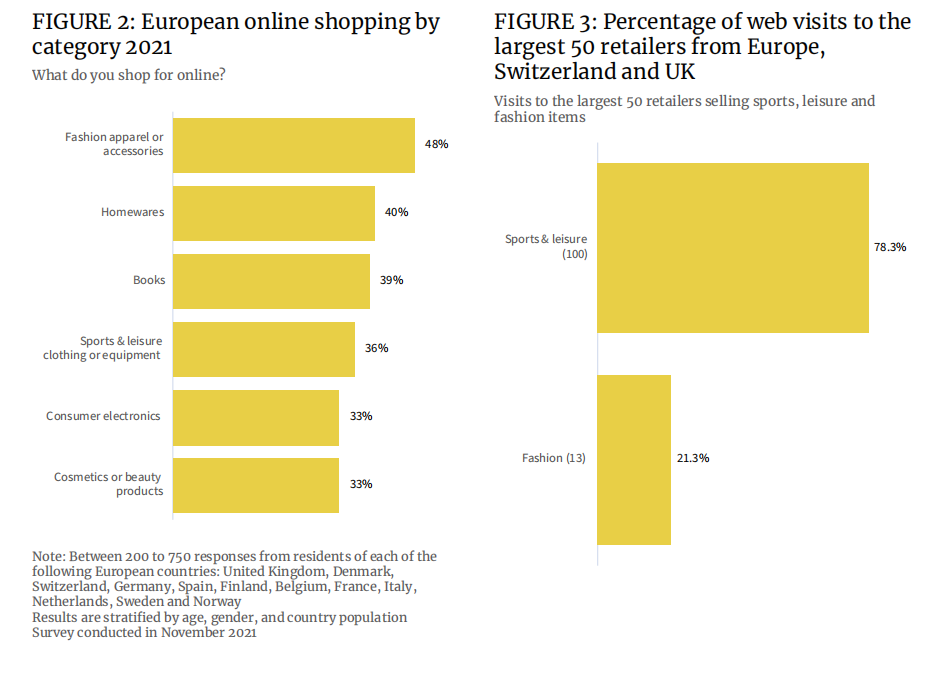

Gögn sýna að árið 2021 munu 36% Evrópubúa kaupa íþrótta- og tómstunda fatnað & Búnaður á netinu og hlutfall verslunar á netinu í þessum flokki er aðeins aðeins á bak við bækur (39%) og heimilisvörur (40%). Netverslun fyrir tískufatnað & Aukahlutir voru 48%, sem bendir til þess að heildarinnkaup á netinu neytenda á þessu svæði sé lægra en á öðrum svæðum.

Hvað varðar hlutfall heimsókna til 50 efstu smásalanna í Evrópu, leituðu meira en 78% að leitarorðinu “Íþróttir og tómstundir”, meðan aðeins 21% leituðu að “Tíska” einn. Þetta þýðir að íþróttafatnaður, athleisure og íþróttatíska verður hluti af fleiri og fleiri fatamerkjum’ Vörulínur.

Á sama tíma hafa heilbrigðisprófanir og líkamsræktarforrit sem segjast bæta meðvitaða hreyfingu fólks sett af stað aðra líkamsrækt “Bylting”.

Mörg fyrstu línuíþróttamerki hafa búið til sín eigin líkamsræktarforrit, staðfest notendasamfélög og hvatt notendur til að æfa meðan þeir opnuðu nýjar tekjuöflunarleiðir, þar á meðal greiddar áskriftir. Nike's Run Club appið er með 15,4 milljónir niðurhals árið 2020, sem er 45% aukning miðað við 2019 og hefur orðið mikilvægari hluti af tekjuskipulagi Nike. Greiningin sýnir einnig að appið hefur fært mjög mikla útsetningu fyrir Nike í samskiptasamfélagi úti íþróttanotenda eins og Running. Léleg en hágæða vörur Nike búnar “Svart tækni” hafa verið seldir á háu verði.

Þessi forrit safna röð líffræðilegra gagna frá notendum, svo sem hæð, þyngd, aldur, fatnað og skóastærð o.s.frv., Og skráningarbreytingar á ýmsum vísbendingum um líkamsrækt, þ.mt hjartsláttartíðni meðan á æfingu stendur. Þetta eitt og sér fær þessi vörumerki ávinning. Ástæðan er sú að vörumerki geta veitt notendum persónulegri tillögur um kaup byggð á gögnum. Árið 2021 mun meðalútgjöld í greiddum líkamsræktarforritum í Evrópu aukast úr $ 41 árið 2017 í $ 60 og er búist við að það muni halda áfram að vaxa á næstu 10 árum.

Að auki hafa sjálfbær hugtök einnig áhrif á neytendur’ Verslunarákvarðanir.

Gögnin sýna að um 5% íþrótta- og tómstundaafurða sem neytendur keyptu árið 2021 eru byggðir á sjálfbærum þróunarástæðum (4,5% hjá körlum og 5,4% hjá konum), þó tiltölulega lítið, samanborið við 3,8% árið 2019. Í samanburði við 4,6% kvenna hefur hlutfall karla verið bætt. Í lok árs 2022 gæti sala á sjálfbærri íþróttavöru orðið 4,9% (karlar) og 5,9% (konur).

Í evrópskum íþróttavörum er markaðsvirði sjálfbærra vara um 600 milljónir evra árið 2021 og getur orðið 800 milljónir evra árið 2022.

Fyrirtæki bera nú ábyrgð á að kanna nýtt, sjálfbær efni og gera framleiðslu sína, flutninga og umbúðir eins sjálfbærar og mögulegt er. Birgjar, framleiðendur og vörumerki munu einnig fylgjast betur með endurvinnslu efna og knýja fram gjalddaga notaða íþróttavörumarkaðarins.

Þrátt fyrir að sjálfbærar vörur treysti á efni, tækni og framleiðsluferli og séu efnislegar og orkufrekar, eru áhorfendur þeirra hneigðari til að greiða iðgjald fyrir sjálfbæra vörur og eru 64% svarenda. Þetta mun hvetja iðnaðinn til að auka fjárfestingu í samræmi við það til að laga sig að eftirspurn á markaði.

Til dæmis hefur Nike, síðan 2019, gert sér grein fyrir því að hægt er að endurvinna eða breyta 99,9% af úrganginum í skóframleiðslu eða breyta í aðra orkugjafa. Síðan 2016 hefur Nike dregið úr notkun ferskvatns um 23 milljarða lítra á ári. Annar risi í greininni, Adidas, sagði á vefsíðu sinni að frá 2020 yrðu 60% af vörum sínum gerðar úr sjálfbærum efnum. Vörumerki eins og Patagonia eru sjálf í stakk búin til að vera umhverfisvæn og sem neytendur’ Áhugi á sjálfbærum vörum eykst, sala hækkar einnig.

Fjöldi nýrra vörumerkja hefur einnig komið fram. Lífræn grunnatriði, kærasta safn og Wolven hafa öll orðið vinsælli síðan 2020 og Sportsshoe, faglegt rekstrarskófyrirtæki, hefur endurskipulagt viðskipti sín hart til að bregðast við markaðsþróun til að ná titlinum “Grænustu, endingargóðu hlaupaskór heimsins” Titill.

- Þróun neytenda

1. persónuleg hreyfing

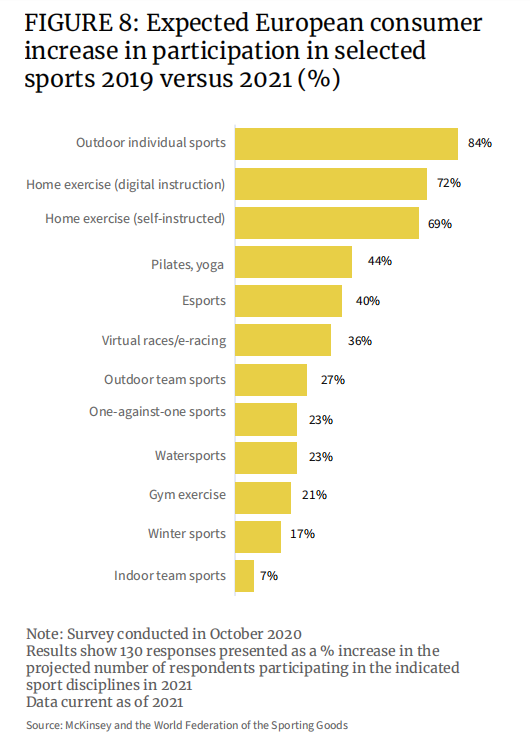

Samkvæmt gögnum sögðu um 65% svarenda í Þýskalandi, Ítalíu, Spáni og Bretlandi að eftir faraldurinn myndu þeir samþætta persónulega heilsu sína í daglegu lífi sínu. Leiðin er hreyfing. Niðurstöður könnunarinnar sýna að samanborið við 2019 verða íþróttamennirnir sem Evrópubúar eru meira hneigðir til árið 2021, persónulegar útivistaríþróttir verða með þeim bestu, með 84% aukningu innan tveggja ára, líkamsrækt innanhúss (eftirfylgni á netinu) mun aukast um 72%, rafræn íþróttir og sýndaríþróttir. Motorsports virkni hækkaði einnig umtalsverðan vöxt, jókst um 40% og 36% í sömu röð.

2.. Afkastamiklar vörur

Notendur sem elska afkastamiklar vörur skilja að þeir eru að kaupa rekstrarvörur, svo sem hlaupaskóna. Eftir 500 mílur af sliti byrja stuðnings froða og slitlag að slitna og höggþolið er ekki lengur til staðar; Swite-wicking fatnaður notar pínulitla silfurþræði til að hjálpa til við að svitna svita og halda fötum þurrum, með takmarkaðri virkni; og íþróttabrasar það missir mikilvæga stuðningsaðgerð sína eftir endurtekna notkun. Byggt á þessu eru notendur afkastamikilla vara yfirleitt tryggir endurteknir kaupendur. Með vinsældum hugtaksins heilsu opnaði sala slíkra vara smám saman.

3. Íþróttir

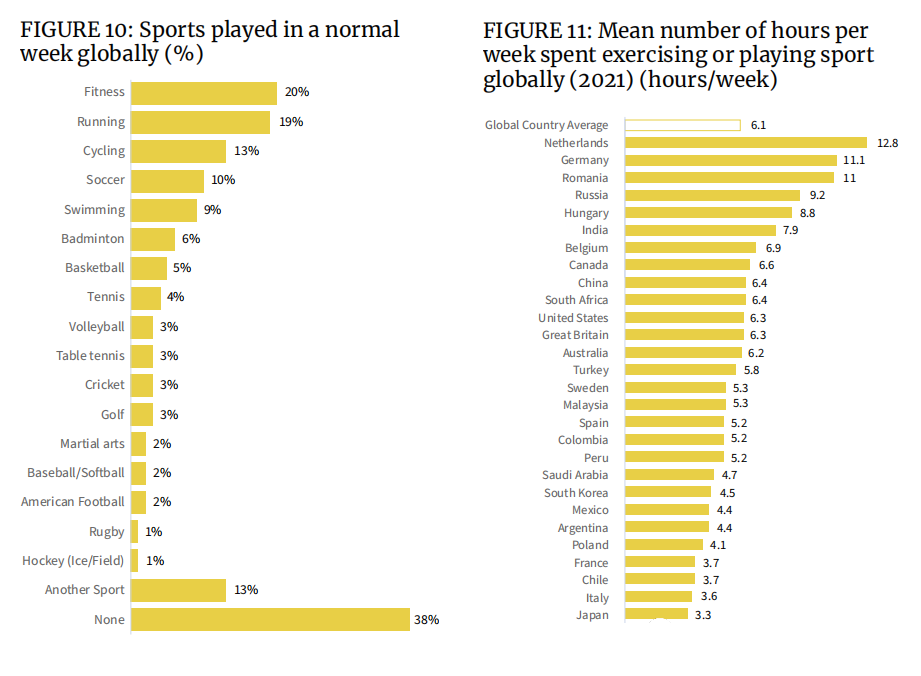

Eins og þú sérð á myndinni hér að neðan, eru líkamsrækt, hlaup og hjólreiðar topp 3 vinsælu íþróttirnar um allan heim. Liðsíþróttir eins og fótbolta, körfubolta, blak og krikket, svo og einn-á-einn boltaíþróttir eins og badminton, tennis og borðtennis, eru einnig að verða sífellt vinsælli og auka sölu á sérhæfðum fatnaði, skóm og búnaði.

Frá sjónarhóli vikulegs æfingatíma er fólk á Spáni og Ítalíu í Evrópu ekki mjög áhugasamt um að æfa. Um það bil 16% Ítala og 14% spænskra svarenda sögðust hafa áhrif á veður. Frá samfélagslegu sjónarmiði hafa bæði löndin orðið fyrir barðinu á heimsfaraldri og ólíkt öðrum löndum í Evrópu sjá líkamsrækt og líkamsrækt sem lykillinn að heilbrigðum lífsstíl.

4.. Kaupval

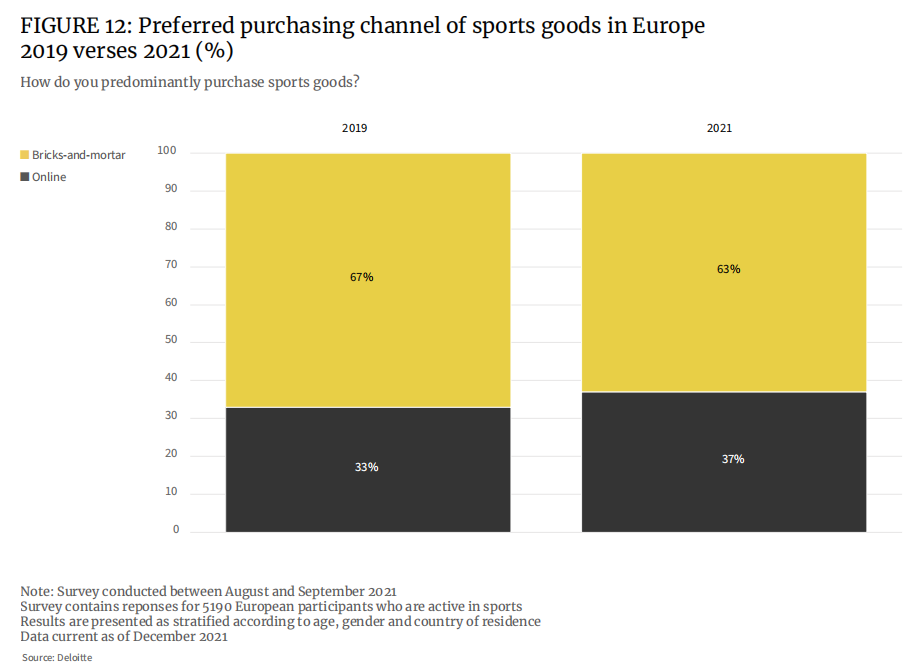

Fyrir faraldurinn kusu 67% svarenda líkamlegar verslanir að kaupa íþróttavörur. Árið 2021 lækkar það hlutfall í 63 prósent.

Fyrir faraldurinn var hlutfall Evrópubúa að versla íþróttavörur á netinu 33% og það mun hækka í 37% árið 2021. Fleiri vöruval og hærri kostnaðarárangur á netverslun eru meginástæðurnar fyrir aukningu á hlutfalli netverslunar.

Hins vegar má sjá að líkamlegar verslanir eru enn fyrsti kosturinn fyrir flesta Evrópubúa til að kaupa íþróttavörur, svo sem nokkra dýrar atvinnuíþróttaskór, eða sérsniðna stíl, sem krefjast þess að neytendur komi í búðina, svo og gauragang eða geggjaður og annan búnað. Það þarf að upplifa útlit og árangur í versluninni áður en þú getur keypt með sjálfstrausti.

- Vinsælir flokkar

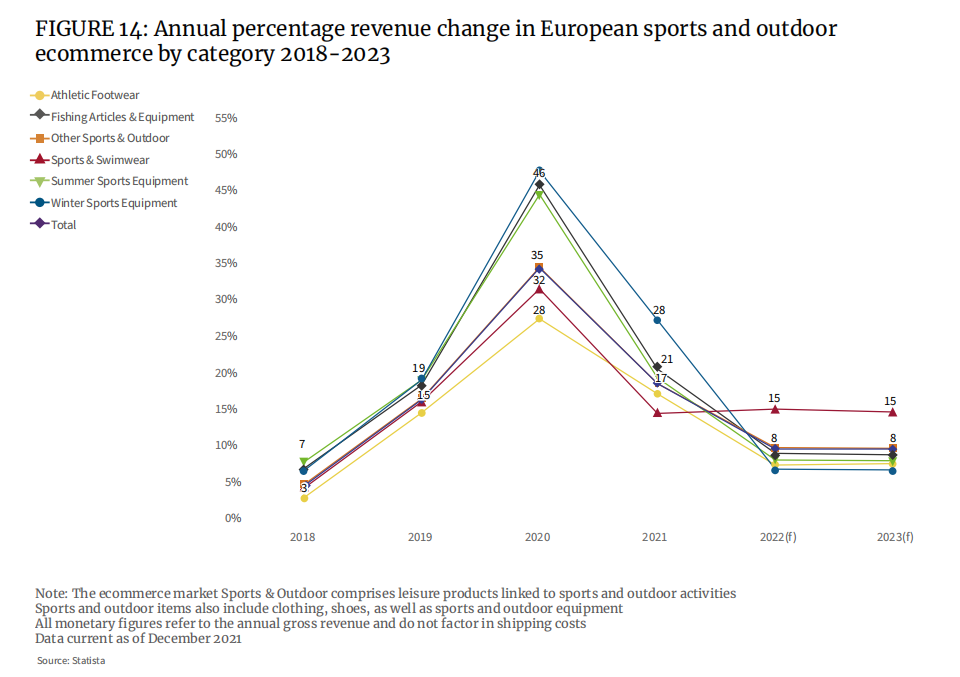

Markaðsgögn sýna að sala á öllum markaðssviðum, frá strigaskóm, veiðibúnaði og sundfötum, hefur aukist árið 2020. Meðalhagnaður allra flokka náði hámarki 35% á þessu tímabili.

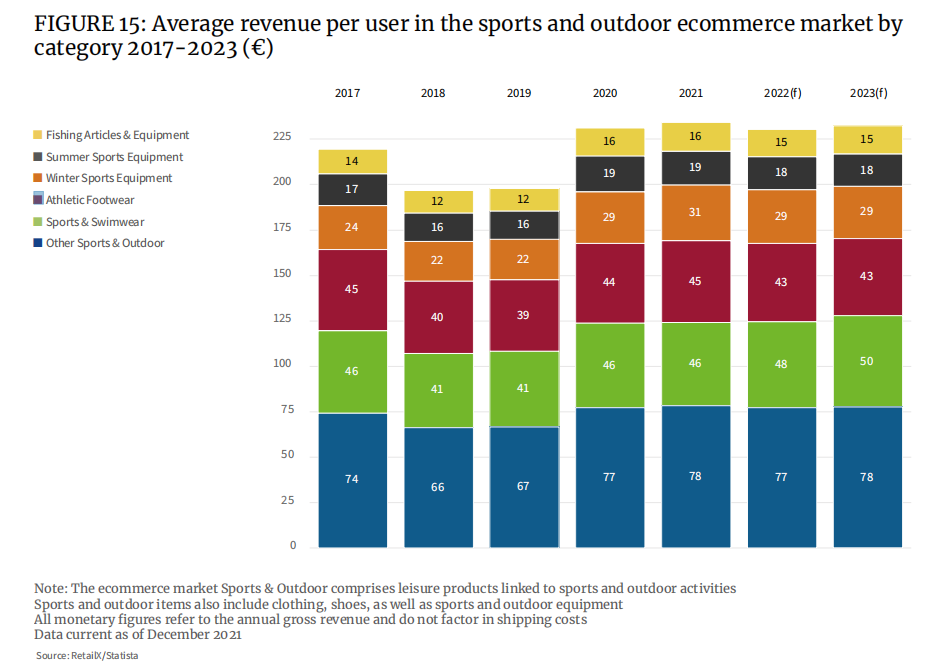

Það var augljóst á heimsfaraldri að útgjöld neytenda í veiðum, persónulegum íþróttum og öðrum íþróttabúnaði úti hefur aukist mikið. Team íþróttabúnaður og skór eru á hinn veginn. Meðaleiningarverð á einum neytanda sýnir að frá 2019 til 2020 hefur neysla á veiðum og öðrum útivistaríþróttum aukist verulega. Meðaleiningarverð á veiðum hækkaði úr 12 evrum í 16 evrur og meðalverð einingarverðs annarra útivistar stökk úr 67 evrum í 77 evrur, sem var 33% hækkun og 15%.

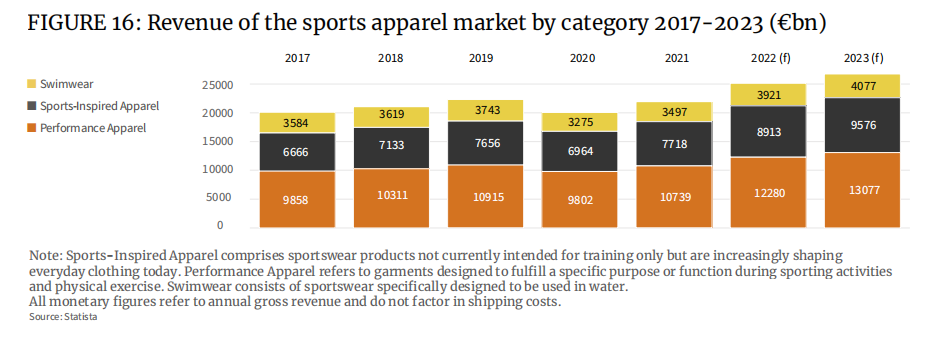

1. íþróttafatnaður

Hægt er að betrumbæta íþróttafatnað í afkastamikið íþróttafatnað, smart íþróttafatnað o.s.frv., Sérstaklega það síðarnefnda, sem hefur smám saman tekið á sig mynd sem þreytandi stíl síðan á sjöunda áratugnum, og íþróttamerki eins og Fila, Adidas Originals, Champion osfrv. (Eða vöru útibú). ) tilheyra þessum stíl. Eftir faraldurinn hefur íþróttaföt eins og jógaföt verið samþykkt af fleiri og fleiri og hafa orðið dagleg slit. Þetta knýr beint vöxt tískusíþrótta, sem mun ná 7,7 milljörðum evra árið 2021 og geta hækkað í næstum 9 milljarða evra árið 2022.

2.. Útiskór

As a sub-category of the outdoor functional clothing market, the market value of outdoor sportswear shoes in Europe is about 3 billion euros, accounting for about half of the market value of the outdoor industry, and it is expected to achieve strong growth in the future. After the epidemic, people are increasingly yearning for the outdoors, and the purchase of outdoor clothing and equipment for hiking, camping and mountaineering has surged. In the past, this was a luxury, but for more and more consumers, it has become a hobby and a pastime.

Bikes have also seen a surge in demand in 2019, 2020 and 2021. The European bicycle market grew by a staggering 40% in 2020 to €18 billion. Against this backdrop, the European cycling apparel market will also grow by 6% between 2020 and 2026. In Europe, there is a growing interest in using bicycles as a daily means of transportation.

3. Sports shoes

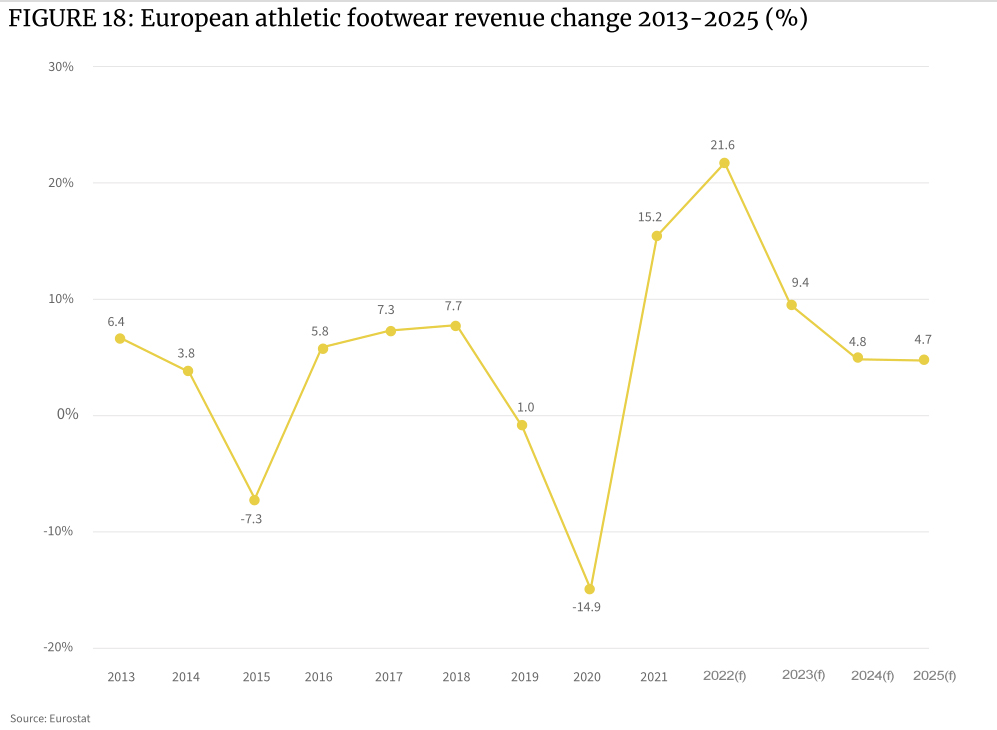

Sneaker sales in Europe plummeted during the coronavirus lockdown in 2020 as many sports venues used for professional sports were forced to close. However, the ensuing rebound in 2021 is astounding, with revenue for the category across the continent growing by 15.2%, and a further increase to 21.6% in 2022.

The epidemic has stimulated consumers’ Verslunarþrá, sérstaklega yngri hópurinn á markaðnum, sem eru áhugasamir um heilbrigðari lífsstíl, þannig að fleiri taka alvarlega þátt í íþróttum. Einnota tekjur fólks aukast og það hefur svo mikill áhugi á réttum skóm til að klæðast fyrir hverja íþrótt.

Nýkomin líkamsræktarforrit eru einnig að vekja áhuga á íþróttum og gegna hlutverki í því hvernig á að velja rétt skófatnað sem og upplýsingar um að koma í veg fyrir meiðsli og bæta íþróttaárangur. Þetta rak enn og aftur sölu á afkastamiklum íþróttaskóm á markaðshliðinni.

Allur evrópski skófatnaðurinn er um 130 milljarða evra virði, þar af er íþróttamarkaðurinn um 50 milljarða evra virði og íþróttamarkaðurinn og úti skófatnaður er 48 milljarðar evra virði.

4. Sundföt

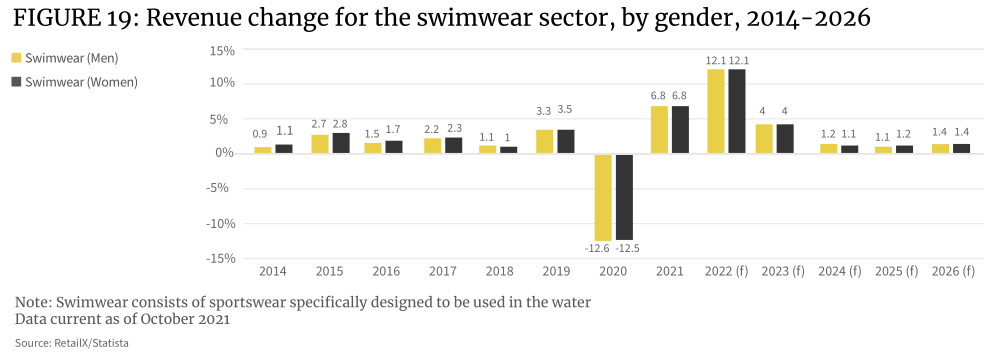

Gert er ráð fyrir að vöxtur sundfötamarkaðarins muni ná 12,1% árið 2022 og sumum af uppsagnarprófi og eftirspurn eftir ferðum verður sleppt. Hluti mun síðan koma á stöðugleika yfir stigum 2019.

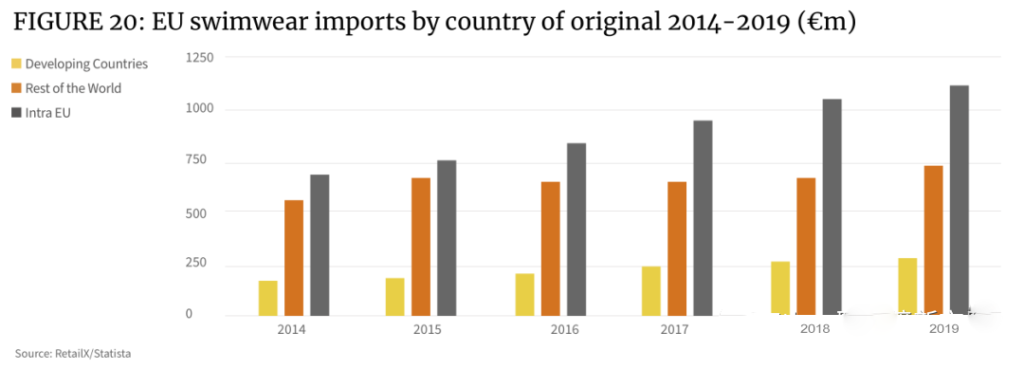

Verðmæti innflutnings á sundfötum ESB hefur aukist á árinu 8,5% undanfarin fimm ár, hærri en meðalvöxtur 5,8% fyrir allan innflutning ESB fatnaðar. Árið 2019 var innflutningur á evrópskum sundfötum 2,1 milljarður evra að verðmæti úr 1,4 milljörðum evra árið 2014

Germany (295 million euros), France (176 million euros), the Netherlands (171 million euros), Italy (166 million euros), the United Kingdom (157 million euros) and Poland (109 million euros) are Europe’s largest exporters of swimwear. The total export market size of swimwear clothing in these six countries accounts for more than 70% of the overall EU market.

5. Sports and leisure wear

Athleisure has become a key trend ahead of 2019, and the work-from-home mandate has kept sales growth strong in 2020 and 2021 and shows no signs of slowing down.

Casual sportswear has become not only a specialized segment of sportswear, but also an alignment target for fashion brands. Therefore, the line between sportswear and fashion clothing is also rather blurred.

The changing shopping habits of many consumers place a healthy lifestyle above other pursuits and make physical activity part of their daily routine. For example, wearing sportswear to Zoom meetings has become more widely accepted in many business areas.

The rise of fitness software and corresponding supporting services during the epidemic has also prompted more consumers to accept sportswear in their daily lives and actively engage in sports on weekdays.

As a result, the sportswear industry is quickly combining it with the fashion forward of clothing to create garments that meet the needs of fashion, leisure and sports, enabling the growth of this new product segment.

Other factors have also shifted the focus of the fashion industry towards athleisure. In 2020, the online sales of DTC sports brands will increase, and the cooperation between social media and self-media practitioners has gradually become an important marketing method.

At present, the main players in the sportswear market are Nike and Adidas. Later new entrants, Under Armour and Lululemon, both have pre-eminent market positions in the pantheon of sportswear fashion.

6. Sports equipment

The size of the sports equipment market has experienced shrinkage in 2020 and then experienced rapid expansion in 2021. The expansion rate of this category market is expected to level off in 2022.

Tennis equipment is a good reference indicator. Europe owns 52% of the world’s tennis clubs, and the European tennis racket market will be worth 103.55 million euros in 2021 and is expected to reach 114.13 million euros in 2028, with a CAGR of 1.4%.

Also worthy of attention is the football equipment market. The global football equipment market size was valued at USD 1.9 billion in 2019 and is expected to reach USD 3.7 billion by 2027. The global market is expected to grow at a CAGR of 18.3% from 2021 to 2027.

Evrópski líkamsræktarmarkaðurinn hefur aukist á heimsfaraldri og þó að hann muni halda áfram að vaxa í framtíðinni mun hann sýna veikleika hraðar en aðrar tegundir íþróttabúnaðar. Markaðurinn á líkamsræktar- og líkamsræktarbúnaði er metinn á 2 milljarða evra árið 2021 og mun vaxa með 3,1% árlega milli 2021 og 2031.

- Svæðishagkerfi helstu íþróttamarkaða í Evrópu

Evrópa er heimili margra heimsþekktra íþróttamerkja, þar á meðal Adidas, Puma og Fila. Á sama tíma eru vesturlenskir markaðir eins og Þýskaland, Frakkland, Ítalía, Spánn, Bretland og Holland ráðandi álfunnar. Aftur á móti er mið- og Austur -Evrópumarkaðurinn minni en hefur meiri vaxtarmöguleika.

An analysis of the shopping patterns of European sports consumers found that less than 10% of consumers across the region actively buy sporting goods online. The main reason is that consumers prefer the shopping experience of a brick-and-mortar store when purchasing sporting goods. While the pandemic has prompted a surge in online sales across industries, online retail sales of sporting goods have grown relatively slowly.

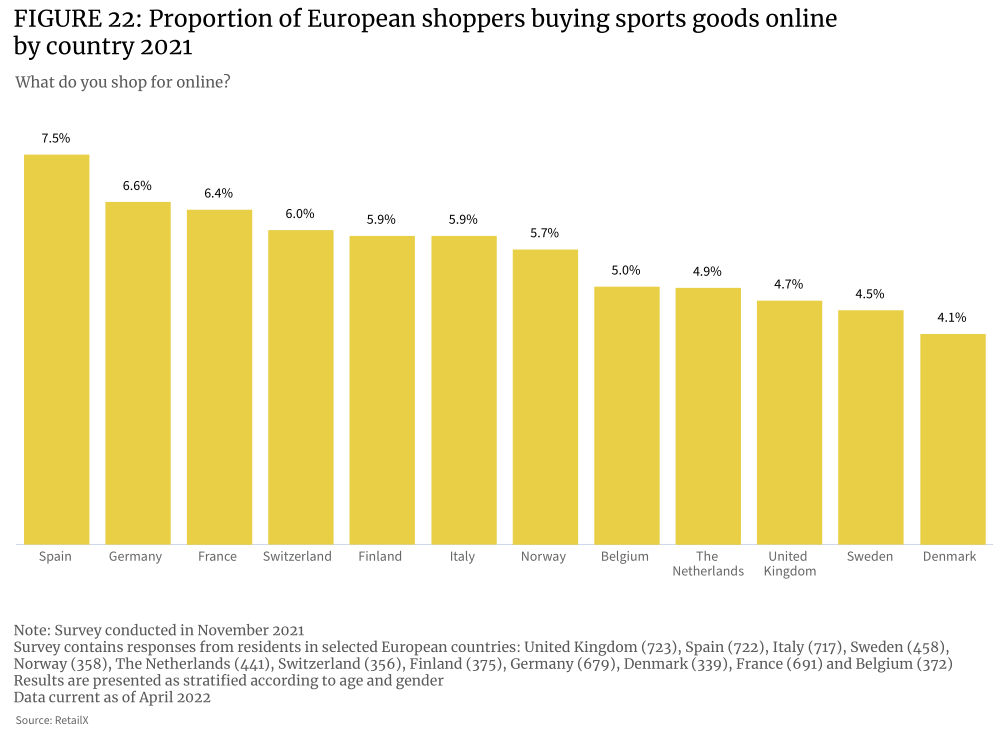

Interestingly, among the online consumer groups, sports consumers account for the largest proportion (7.5%), and Spain is one of the countries in the European Economic Area that use sports as a pastime. The sports e-commerce category penetration rate in the Netherlands is relatively low (4.9%).

Many consumers want to shop in-person for sporting goods and equipment in brick-and-mortar stores. In sports-oriented countries, consumers are more focused on finding the right professional gear and apparel. In markets where sports are less developed, the opposite is true, where consumers have higher e-commerce participation rates (eg Spain).

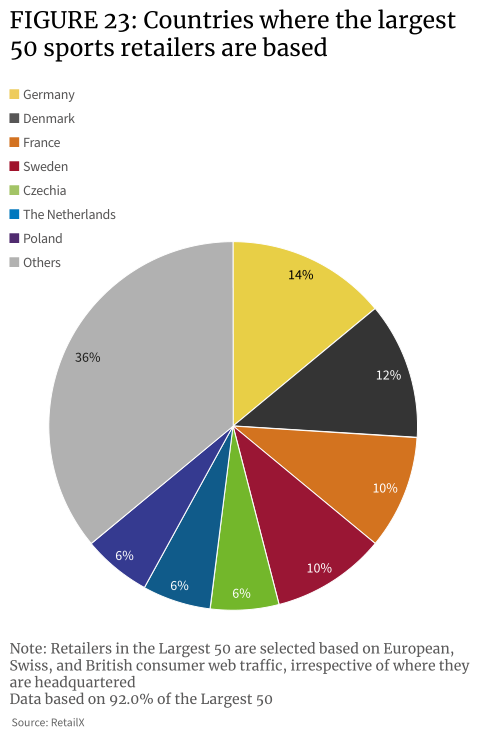

Germany and Denmark have the highest concentration of online traffic among the TOP 50 sports retailers, accounting for 14% and 12% of the overall market traffic in Europe, respectively. Germany ranks second in the number of online sports consumers. In the Netherlands, which has the largest number of sports consumers, its online sports retailers account for only 6% of the traffic.

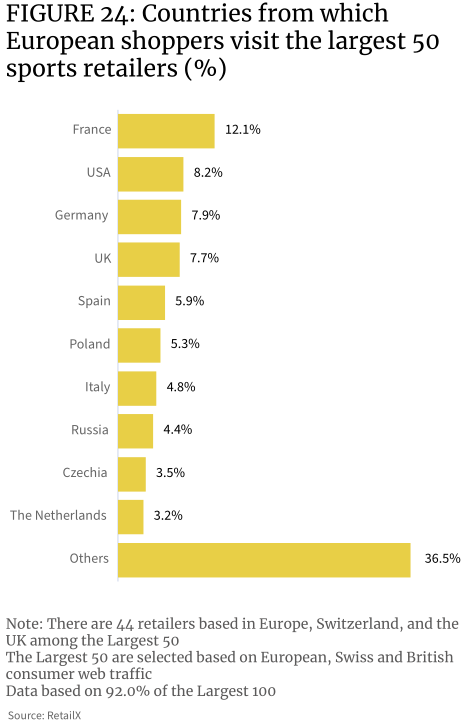

The data shows that the sports category has a relatively strong performance in the cross-border market. For example, the top 50 sports retailers capture 7.9% of German consumers, and 14% of these retailers are headquartered in Germany. Likewise, the top 50 sports retailers capture 12% of French consumers, of which only 10% are headquartered in France. More than 8% of the TOP 50 sports retailers’ website traffic comes from the United States.

This also shows, to a certain extent, that the European online sporting goods and equipment market is less affected by national borders than other retail categories.

Even the UK, where there may be additional barriers to buying from the EU post-Brexit, has a whopping 7.7% of visits to TOP 50 retailers by local consumers, suggesting that many UK consumers are still on European e-commerce sites When buying sporting goods, UK sports consumers have always valued EU specialist brands and retailers.

Europe is a major supply and marketing market for sporting goods and equipment, with imports increasing between 2015 and 2020. Compared with 2015, both imports and exports have increased in 2020, and the growth rate of imports (37.8%) is higher than that of exports (28.2%), with an increase in imports of about 3.7 billion euros and an increase in exports of about 2.6 billion euros . As of 2020, Europe’s exports were 11.8 billion euros and imports were 13.5 billion euros.

European sneaker exports are growing, with a 74% increase between 2015 and 2020. Most of these exports go to the United States, Japan, China, Russia, South Korea, Turkey, Canada, the United Arab Emirates, Ukraine and other countries. Among them, the largest decline in exports was snowboards, which fell by 5% year-on-year.

The number of boats and water sports equipment imported into Europe is increasing, increasing by 155% in the five years to 2020. Imports of gymnastics, sports and swimming equipment also surged, up 33% over the same period.

In 2020, in terms of value, Germany and the Netherlands were the EU’s leading exporters of sporting goods, with exports worth around 5.3 billion euros, followed by Italy (4.4 billion euros) and Belgium (3.6 billion euros). The main importers in Europe are Germany (6.3 billion euros), the Netherlands (4.7 billion euros) and France (3.7 billion euros). Italy, which has a sizable trade surplus of 23 billion euros, exports almost twice as much sports-related goods and equipment as it imports.

Intra-EU trade in sporting goods is strong, with imports from within the EU and imports from outside the EU accounting for 51%:49%. The import of fashion sportswear within the EU is dominated by Germany, which accounts for 11.7% of the market share, equivalent to a market value of 1.8 billion euros. This is followed by Italy (5.7%), the Netherlands (5.3%) and Belgium (4.9%).

Meanwhile, Poland is a national market to watch. It has one of the fastest growing imports of sporting goods of any country in continental Europe, has a large and increasingly affluent consumer base, and is one of the emerging online retail markets.

- European Sporting Goods Market Competitive Landscape

Sporting goods are sold through retailers, stores and distributors across Europe, with the market segmented between specialty stores, general sports retailers and brands. The marketplace is also increasingly in play, and the industry is also seeing indirect and digital competition from other industries, such as fashion brands, department stores and other retailers.

Large integrated sports retailers constitute the dominant retail landscape of the market, consisting of retailers selling a wide range of sports and recreational sporting goods, catering to a large customer base. However, they remain focused on outdoor sports and are therefore able to offer products to consumers who focus on performance and recreational sports. Key market competitors in Europe include Decathlon and Sports Direct. These retailers, which have traditionally been brick-and-mortar stores, have gradually opened up to the e-commerce space and are now focusing on omni-channel business models.

Mainstream platforms such as Amazon and eBay have long been major sporting goods sellers, and well-known brands such as Adidas and Nike have also opened their own branded stores on e-commerce platforms to sell end products and other merchandise to avoid cannibalization. Retailers such as Decathlon have gone a step further by opening their own marketplaces to enhance their core expertise and expand their reach into the wider sporting goods market. Other, more specialized platforms that cater to specific sports and categories are also emerging.

The European sporting goods market is served by a range of online and omni-channel retailers, with at least one major player in the top 100 in each country. For example, Germany has several ball retailers appearing in the rankings, representing a certain size in the sports and outdoor goods and equipment market, which is also the development of cross-border e-commerce with countries such as Switzerland, Austria, Poland and the Czech Republic. result of development. In contrast, the UK has only one retailer (Sports Direct) in the top 20.

The distribution of European retailers is also influenced by some well-known brands, usually brand giants such as Nike and Adidas to promote cross-border sales through other retailers and brand stores around the world.

- Growth points of the European sports industry in 2022

Like all retail verticals, sports shoppers in Europe have seen dramatic changes in their shopping habits throughout the pandemic, but perhaps not as dramatically. In sporting goods, the shift in consumer behavior to online shopping has been far less dramatic than in other areas, while the return to brick-and-mortar retail has been more rapid.

So what are the growth points and trends of European sporting goods in 2022 and beyond?

The epidemic has made more consumers in Europe pay attention to their health, thanks to the strong focus on fitness among young people and the growing influence of the fitness industry. Paradoxically, Europe’s obesity crisis is also growing, and governments are starting to take action to curb it.

A 2020 UK study found that eight times as many teenagers are exercising to lose weight than in 1986. When surveyed last year, 6 in 10 14-year-olds said they exercised to lose weight, compared with just 7 percent in 1986.

Millennials and Gen Z make up 80% of the overall fitness club membership, while 85% of gym members also exercise at home. 89% of people aged 16 to 34 use fitness apps to exercise.

As these young users continue to exercise and resume team sports and other activities that have been curtailed during the pandemic, this will further drive growth in sporting goods sales.

The fitness industry is also being driven by the Gen Z and millennial cohorts as they focus not only on fitness but also on overall physical and mental health. From 2017 to 2021, the global health industry market size has grown by 6.4%, with a market value of approximately $3.7 trillion.

Fitness is just one key area of that. The growth of the wellness industry directly drives the growth in the purchase of sporting goods, especially footwear, apparel and sports equipment, and promotes related technology upgrades.

Childhood obesity is on the rise in southern European countries. The figures show that in Cyprus, Greece, Italy, Malta, San Marino and Spain, around one in five boys (ranging from 18% to 21%) are obese.

This is where the government is taking action to improve children’s health and encourage people to participate in sports and exercise. This will lead to an increase in the demand for sporting goods in the entire European market, and the business opportunity can be described as self-evident.

At the same time, Gen Z and millennials are driving growth in the sports and fitness industries. Younger groups account for more than 65% of the overall proportion of virtual fitness users. The main consumer groups are eager for a seamless and interconnected fitness experience. The experience provided by merchants needs to adapt to people’s lifestyles and match different sports scenarios. Therefore, fitness software that incorporates virtual technologies such as AR, and the corresponding fitness equipment/technology can attract consumers’ attention more than ever.